You will hear the term credit utilization a lot when looking at car loans. It’s a term you’re going to want to get to grips with if you want the best loan for your situation.

So what is credit utilization for car loans and why should you care?

What is Credit Utilization?

Credit utilization is a ratio used in car loan calculations. The term refers to how much debt you have compared to your income. The higher the debt, the higher the debt ratio.

The higher your debt ratio, the more cautious a lender will be when considering you for a car loan.

Credit utilization has two elements. The most common is the individual ratio for credit cards. It is designed to assess how close to your credit limit you are. A second, general ratio is used for your overall credit.

Why Should You Care About Credit Utilization?

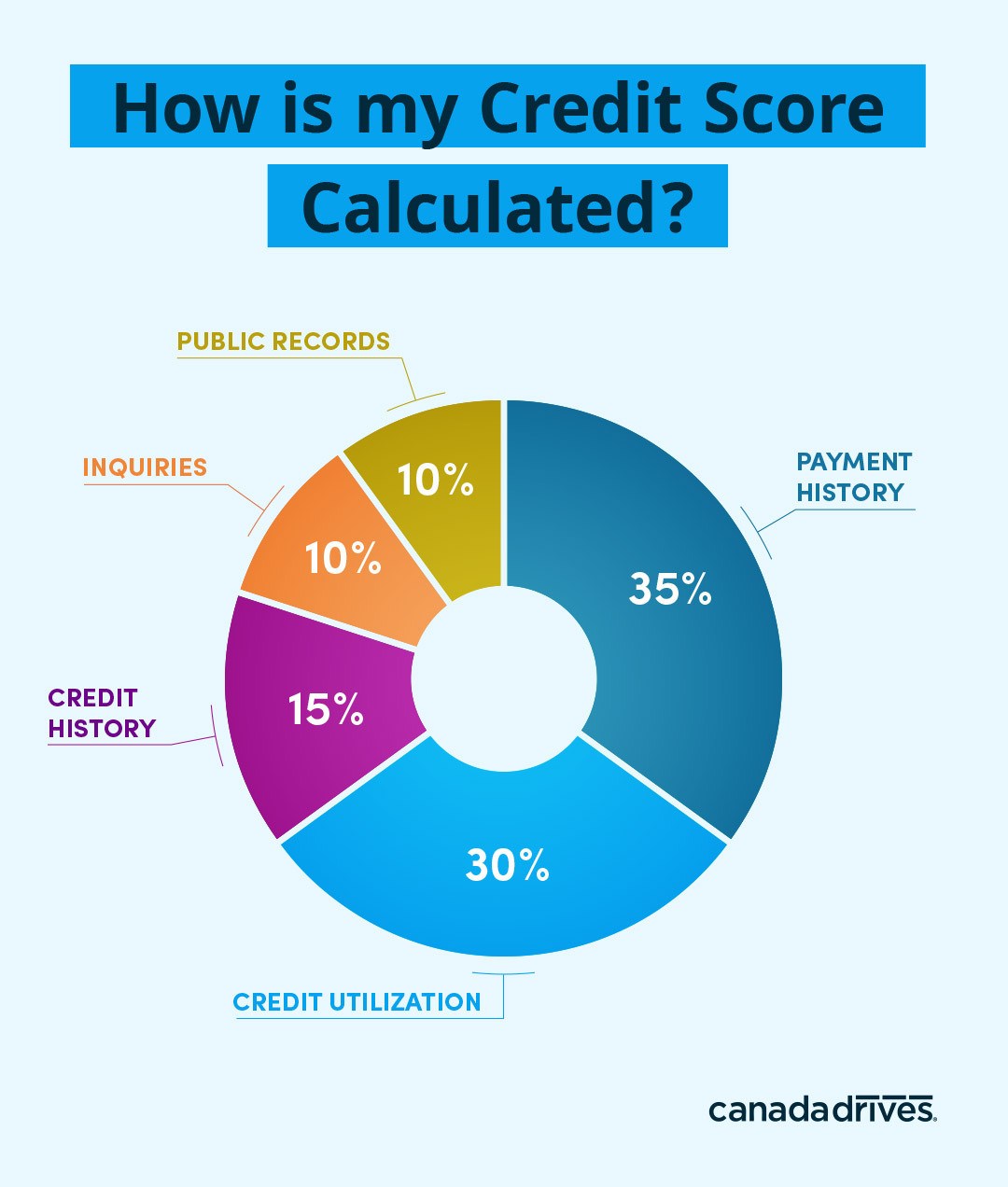

Depending on the credit reference agency you talk to, your credit utilization ratio value can make up to 30% of your credit score. It is second only to your payment history in terms of influencing your credit score.

That’s why you should care about credit utilization.

There is no ‘perfect’ credit utilization ratio. An average of around 30% is regarded as normal. That means your current debt is only 30% utilized for credit cards or 30% of your available monthly income for general lending.

How to Calculate Your Credit Utilization Ratio

If you’re considering a car loan, it might help to know your credit utilization in advance. We can help you do that if you like but you can also do it yourself.

Check your credit cards to see how close to the credit limit you are. Translate this into a percentage to get your number. For example, if you have $500 on a credit card but your credit limit is $10,000, your ratio is just 5%. ($500 / $10,000 x 100).

If you have other borrowing, you can perform a similar calculation of monthly debt versus monthly available income. We can help you with this if you need us to.

Managing Credit Utilization

The simplest way to manage your credit utilization is to borrow sensibly and make sure you can comfortably afford that car loan. If you want to reduce your ratio, pay off credit cards and pay off any store cards or other expensive debts.

Your credit report won’t reflect those payments immediately as it’s only updated once per card billing cycle. Other debt will likely be the same. Keep it up and your ratio should improve.

Ready for your next car loan? We’d love to help! Click here to get approved today.